Checking out Checkout.com, the payments service provider fast follower

Is there another Adyen out there?

Hi there! Thanks for reading. If you haven’t visited before, check out my post on a soon-to-be-listed company called AvidXchange.

Suggestions from The Suggestivist:

For investors: Checkout is a digitally native payment service provider that is growing faster than its much-loved public comp, Adyen. Checkout cut its teeth helping underserved businesses (and geographies) accept payments and grow, and is now increasingly announcing deals with large, global merchants. The company has no concrete plans to IPO, but I wouldn’t be surprised to see it come public within a year or two. If you own a business like Adyen, this writeup should help you better understand the competitive landscape.

For Checkout: Impressive stuff. But help investors understand: why are merchants moving to you versus Adyen (or others)? Are you cheaper? Do you have better conversion? Also, when eventually going public, I'd be sure to highlight the margin opportunity.

Checkout.com, the payments service provider fast follower

One of the most impressive companies to emerge within the payments landscape over the last 20 years is an Amsterdam-headquartered payments service provider (PSP) called Adyen. For those that don’t know, Adyen helps online companies seamlessly accept payments in countries all around the world. The company’s customer list is a who’s-who of large internet businesses: customers include eBay, Spotify, Uber, Netflix, and many others. Its focus on internet-first businesses challenged existing brick-and-mortar PSPs, which offered inferior solutions to online, multi-national businesses. In fact, Adyen is Surinamese for “start over again” – meaning that the business took an innovative approach to payments, effectively breaking the mold in the process. Adyen’s focus on a massive and growing market has propelled the business, and the company’s chart (and valuation) speaks for itself.

What if I told you that there is another Adyen, quietly building its capabilities as a PSP and raising money from VCs to continue to innovate and grow? Well, there is. The company? Checkout.com. Which roughly translates to “start over again, again,” I think – just not in Surinamese. High-profile backers include DST, Coatue, Tiger Global, Greenoaks, Insight Partners, GIC, and others.

If you’re interested in payments, fast-growing businesses, trends in e-commerce, or surfing CEOs, then Checkout is an important company to understand. Its rapid growth and ongoing success is staggering. It is chasing one of the most popular payments businesses, Adyen. And, one day in the not-so-distant future, it will likely IPO. So what makes Checkout special? Let’s dig in.

Checkout highlights

Second most highly valued private European startup (last round at $15B), following Klarna ($45.6B)

Growing 50%+/yr (2019), "significantly faster" than Adyen according to Deven Parekh (board member at Checkout)

Provides payments solutions in 150+ currencies

1,000+ employees

17 international offices

London HQ

Payments flow

Feel free to skip this first section if you already understand how payments work. At some point in time, I want to write a deep-dive on the topic. But, for now, I think this quick explanation will help those not already indoctrinated.

When you use your credit card to buy something, have you ever wondered what exactly is happening? Whether you swipe, tap, or insert, the customary 3-second "processing" delay and then "payment approved" is so commonplace that it fades into the background of any transaction. But behind the scenes, whether paying for something in person, online, or even via another payment platform like Apple Pay, an immensely complicated and regulated chain of processes occurs in real-time.

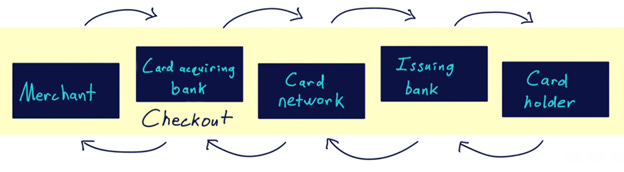

In open-loop card schemes (Visa and Mastercard), there are five key parties that connect through the payments flow. These are the merchant, card acquiring bank, card network, issuing bank, and the ultimate card holder. Checkout sits in the second step, "card acquiring bank." The terminology is a bit confusing, but Checkout can be referred to as an acquirer, processor, PSP, or litany of other names. For the sake of this writeup, I'm going to refer to Checkout as a PSP. The chart below illustrates the payments flow for open-loop card schemes and highlights Checkout’s position within the flow.

To make the payments process more concrete, let's run through the steps in the image above with an example. When I go to my local coffee shop to buy coffee, I tap my card at the merchant's point of sale. This machine, which reads my card, passes information onto the acquirer. The acquirer performs multiple steps (outlined in detail in the next paragraph), but at a high level is in charge of handling authorization message processing for the coffee shop, meaning it communicates to the card networks (e.g. Visa and Mastercard) and confirms or denies payment acceptance. The card network provides the "rails" for communicating transaction details amongst the different parties in the ecosystem, and in this case connects the acquirer to the issuing bank. The issuing bank is the institution that issued my credit card to me, branded with the issuer's logo (Chase) and the network's logo (Visa). Finally, the issuing bank connects to my checking account when I ultimately pay for the credit transaction.

Checkout’s “card acquiring bank” position in the image above is a bit misleading, and in order to better explain what exactly Checkout does, I want to further break down that single step. At a high level, there are two components in acquiring: front-end functions and back-end functions. Front-end acquiring has four sub-steps: 1) the POS vendor, 2) the ISO (sometimes), 3) the gateway, and 4) the front-end processor. The two back-end steps are 1) the back-end processor and 2) the acquiring bank. The image below provides the expanded view of the acquirer.

Let’s run through that coffee purchase again, focusing on Checkout’s role. First, I tap my card at the coffee shop. The card reader is called the “point of sale,” or POS. The POS vendor is straightforward – it is the company that sells a merchant the actual terminal at which cards are accepted. Common POS vendors include Verifone and Ingenico. Once a card is swiped, inserted, or tapped at the POS terminal, the transaction might flow through an Independent Sales Organization (ISO), which runs outsourced card acceptance to certain merchants (really outsourced sales). ISO's are more commonly used by small merchants. The next step, specific largely to online transactions, is that post-tap, payment information flows through a gateway. A gateway is a step that enables and monitors the flow of information in a transaction and can offer value-added services like risk management. Finally, payment details reach the front-end processor, which confirms or denies the transaction and communicates details to the other parties in the payments flow. All front-end functions are done in real-time. Back-end functions are generally settled at the end of day. The two steps in the back end are processing, which means that aggregated real-time payment transaction details (all the coffee sales done throughout the day) are batched, then sent to the second step, the acquiring bank, which handles settlement and billing. Checkout offers acquiring, gateway, and processing services within the acquiring flow.

As is likely very clear by now, a simple card transaction is unbelievably complex and involves the cooperation of a bunch of different parties. It's incredible to think how much heavy lifting is done near-instantaneously just so I can buy a coffee! Before going deeper into Checkout’s unique approach to payments, let’s take a quick breather and look at the origins of the business.

Background

Checkout history: The origins of Checkout are fascinating. Swiss-born, Dubai-based, and now London-working Guillaume Pousaz does not have a stereotypical fintech background (thanks to this Forbes article for providing much of the information in this section). After failing finals in college, Pousaz moved to California to pursue the life of a surfer. He eventually got a job at a US-based payments company close to one of his favorite surf breaks. He worked there for a couple of years, then eventually spun out to start a business with a colleague. Aspirational differences resulted in the dissolution of that business and prompted Pousaz to go solo and pursue his own entrepreneurial aspirations.

Not too long after leaving California, Pousaz purchased a Mauritius-based company called SMS Pay (in November of 2009). Pousaz also setup a new Singapore-based business called Opus Payments that year, which would eventually become Checkout.com. After a couple of years, Opus signed a deal with Chinese website Dealextreme (in 2011), which marked a turning point for the company. In 2012, the rebranded Opus, now called Checkout, was approved by the Financial Conduct Authority in the UK. In 2013, it was granted principal membership to Visa and Mastercard, meaning that Checkout could act as an acquirer and offer processing to customers via these rails. Principal membership was a key milestone in enabling Checkout to grow in Western economies that by and large have high adoption of Visa and Mastercard networks.

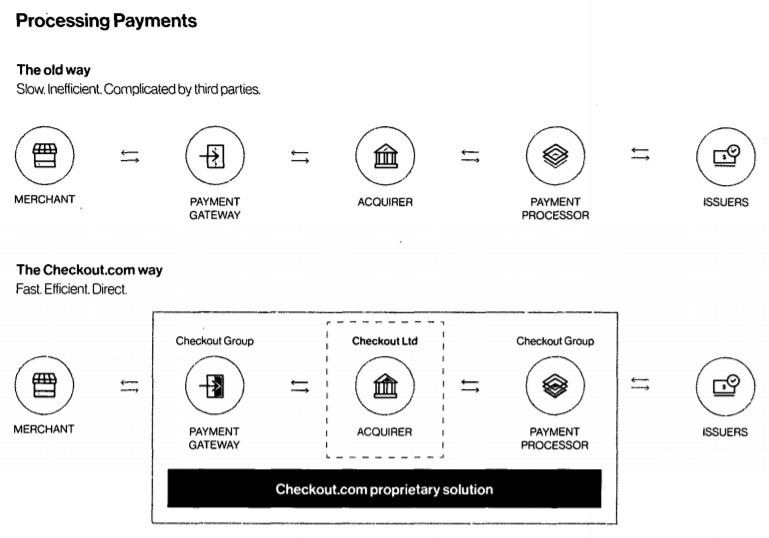

Checkout today: Checkout is a payments acquiring and processing platform (or payments service provider – a term I prefer). Simply put, this means that Checkout connects a merchant (coffee shop) to card networks on behalf of an acquiring bank. Checkout is special because it helps simplify the convoluted payments flow outlined above. Specifically, checkout handles four steps in the payments flow: it functions as a gateway, acquirer, processor, and risk engine (this approach, done through a single software stack, was largely pioneered by Adyen).

The image below, taken from Checkout's filings with the UK's Companies House, illustrates the way in which Checkout consolidates the payments flow. Specifically, the image provides a depiction of two different payments flows. The first, "old way," has five different parties. Merchants would traditionally need to have direct relationships with three of these parties. With Checkout's solution, these three otherwise disparate relationships are collapsed into a single platform. As checkout puts it, the results are that payment processing becomes "fast, efficient, and direct." Checkout calls this propriety solution "connected payments."

Fast follower

Before analyzing the interactions between members of Checkout's business ecosystem, I want to highlight a key feature of Checkout's business model: the company is a fast follower. To set the stage for what this means, let's rewind 15 years.

It is 2006. Fresh off the sale of Bibit (another payments company), Adyen's co-founders, Pieter van der Does and Arnout Schuijff, started a new payments company with the goal of simplifying the payments flow. Their idea? Combine multiple steps (gateway, acquiring, processing) under one roof, with a single, unified code base. This solved two problems. First, handling multiple payment steps made life easier for merchants and helped them grow. Second, the single code base has enabled Adyen to push universal updates to merchants, meaning that changes to fraud monitoring, authorization rules, etc. are all pushed in real time. Merchants would therefore constantly have the best version of a PSP. This is in stark contrast to many other PSPs, which have in large part been built on older software and through M&A, meaning that they could not be updated seamlessly. Adyen's approach proved to be incredibly powerful and successful, especially with large e-commerce businesses.

Fast forward six years: it is 2012, and Checkout.com is formally founded. The value proposition Checkout offers is very similar to Adyen: Checkout operates multiple parts of the payments chain within a single code base. First targeting underserved industries and geographies, Checkout grew, and grew, and grew. Today, Checkout processes transactions alongside Adyen for some of the largest merchants in the world.

I’ve found that many investment analysts tend to quickly underwrite first-mover advantages (in this case, Adyen), but fast followers tend to be less understood. I suspect this is because pattern recognition is difficult to develop for fast followers: they operate in many different industries and appear to employ different growth strategies. Regardless, it is fair to say that Checkout is certainly a fast follower and is replicating the Adyen playbook. As a result of the fast follower dynamic, this report uses Adyen as a point of reference for multiple Checkout initiatives.

Business ecosystem

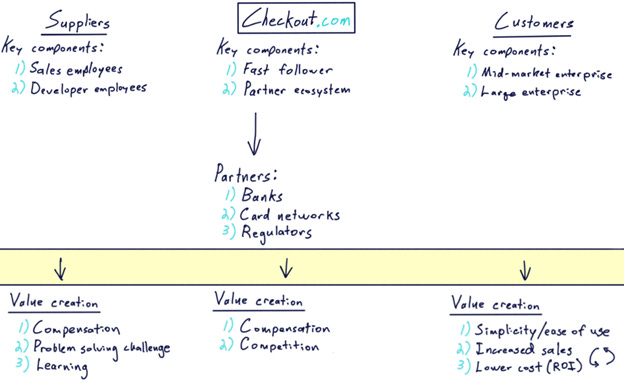

In this section, I zero-in on Checkout’s role in the payments chain and provide a high-level overview of its business ecosystem. I’ve created the image below to help illustrate the key players and how value is created in the ecosystem.

Let’s take a look at how Checkout manages the health of its ecosystem by adding value to each party it interacts with.

Supplier value creation: Checkout employs two important groups of people: those working in sales and those working in software development.

Sales employees: I don’t have much to say about the value creation for sales employees. I’m assuming that they are handsomely rewarded, though, given Checkout’s multi-year growth run. If anybody can tell me more about the life of a sales rep at Checkout, please let me know.

Developer employees: Reviews on Glassdoor are largely positive from developers. Common descriptions of the workplace detail how employees are motivated and kind, work on interesting projects, and have good in-house tech to work with/ on. There also appears to be an appreciation of psychological safety and the ability to learn as you work (make mistakes and move on). As a developer, these attributes, plus good compensation, represent good value creation.

Customer value creation: The customers Checkout provides its services to are primarily online retailers. Below, I break these merchants into two categories: mid-market enterprises and large enterprises.

Mid-market enterprise: Checkout’s value add to mid-market enterprises is twofold. First, the connected payments approach simplifies the payment ecosystem that merchants interact with, resulting in easier setup, integration, and updates, as well as more data. Second, merchants enjoy higher sales thanks to higher authorization rates, geographic access, and increased data access. So, while Checkout’s primarily goal is technically to processes payments, it actually simplifies the payments flow and increases sales for merchants. On its website, Checkout has a case study about Wise, formerly known as TransferWise. This Wise story clarifies the three ways Checkout can increase sales for merchants. I’ve featured quotes from a product manager at Wise, Aleksandr Povarov, to illustrate how Checkout adds value to mid-market merchants.

Authorization rates: “Working with Checkout.com has allowed us to understand our payment data better and turn it into actionable insights. Checkout.com allowed us to increase our approval rates by a full percentage point. With over 9 million customers and billions in transactions a month, that extra 1% really adds up and has a significant impact on our bottom-line.”

Geographic reach: “Each market also has local scheme requirements, so we needed a solution to cut through the complexities of international payment corridors. Checkout.com offered us robust cross-border capabilities and helped to accelerate the pace of our expansion. It integrates with our existing customer experience and unlocks transfers to billions of cards worldwide through a single API. It’s a game-changer not to need a different integration for every region.”

Data: “Data is key to our business…and Checkout.com allows us to see our payments data at a more granular level than ever before. Having this detailed view of the transactions flowing across our business is game-changing. It’s allowing us to spot trends that we’ve never had visibility into before and make better-informed decisions at speed to optimize our flows and ensure we’re getting full value from every transaction.”

Large enterprise: The value that Checkout provides to large, global enterprises is similar to what it offers mid-market businesses: it helps simplify the payments flow and increases sales for merchants. However, large businesses are generally well-served by existing incumbents, unlike some of the mid-market. Consider Netflix. Netflix uses Checkout, Adyen, and Worldpay, among others, as PSPs. The main justification for running multiple payment processors is that it is critical to have a backup(s) that can handle the full load of the business's payment volume in case the primary provider fails. But why Checkout? I suspect that global, enterprise-scale businesses are using Checkout because it gives them good global reach, adequate processing capabilities, and likely competes on price.

Partner value creation: The partner network that Checkout integrates with connects the company to the other parties in the payments ecosystem that ultimately help facilitate transactions. Therefore, managing the relationships and value-add to these parties is critical. Checkout provides value to three different partners.

Banks: Banks make money when they work with Checkout. The interchange fee associated with every credit card transaction goes to banks to compensate for their 1) cost of payment guarantee, 2) cost of funds, and 3) operating expenses. Checkout helps banks connect to more merchants, which in turn results in more transactions and interchange revenue. Banks also make money on interest charged on credit card balances – a revenue stream that is dependent upon connecting with PSPs that help facilitate transactions.

Card networks: Checkout’s principal membership with card networks, including Visa and Mastercard, enable the business to tap into a massive pool of consumers making transactions. Checkout provides value to card networks by connecting them to merchants, which allows the networks to make money on processing fees and foreign exchange fees, among others.

Regulators: The role of regulators in the payments landscape is complicated, given dynamics around setting interchange, monopoly-like competition, and other factors. Regardless, I think Checkout provides value to regulators in that it is another payments competitor in a consolidating industry, therefore injecting a bit more competition. Regulators tend to encourage competition as it leads to more innovation and better outcomes for customers.

Monetization

The ecosystem analysis above illustrates that Checkout provides ample value to the parties it interacts with. Let’s now look at how Checkout captures value for itself. In filings, the company groups its revenue into two buckets: transaction services and treasury management.

Transaction services: This revenue bucket refers to the 1) settlement fees and 2) processing fees that Checkout earns. Settlement fees include interchange, payment network fees, and other costs incurred from financial institutions – a large chunk of this revenue ultimately passes through to financial institutions. As a point of reference: for Adyen, about 89% of total settlement fees end up going to other financial institutions within the payments ecosystem (which is effectively the difference between gross and net revenue). Processing fees are what the merchant pays Checkout on a per transaction basis. The combined settlement and processing fees charged to the merchant can be referred to as interchange ++ (details here).

Treasury management: This is revenue associated with settling foreign currency transactions. As a global PSP, Checkout handles over 150 different currencies and charges a fee for cross-border foreign exchange translation.

Moat

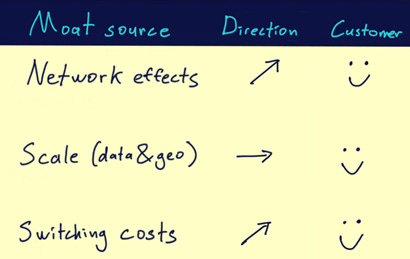

Checkout has a wide moat. What is more important to understand; however, is not the static width of Checkout's existing moat, but rather how the moat will evolve as the company continues to grow. Below, I outline Checkout’s current moat and think through how it will evolve through time, in addition to giving the customer’s perspective on these moat sources.

Network effects: As outlined in the ecosystem map above, global PSPs connect to a number of different partners within the payments world. The three most important parties are merchants, payment networks, and banks. Each time a new merchant, network, or bank is added to Checkout's roster, the value to each other party (theoretically) grows. A quick example: when Checkout won part of Klarna’s processing business, the card schemes, banks, and Klarna all benefited as a result of increased flows and sales. A similar pattern occurs when more traditional merchants join Checkout as well. In this way, Checkout has relatively strong network effects, and replicating all these connections is a real hurdle for newcomers.

Direction: By definition, Checkout's network effects will become stronger as the business grows. As long as Checkout continues to provide adequate value to the members of its ecosystem, this is a net-positive for all parties.

Scale: Checkout has two “scale” moat sources. The first scale advantage Checkout has vs. smaller peers (besides the network effects it enjoys) is its ability to collect data on a large customer and merchant base. The second “scale” moat source concerns geographic, country-by-country regulation of payments. In many cases, entering a new geography as a PSP can take months, or even years. Checkout’s existing ability to process over 150 different currencies in countries all around the world is something that would take a very long time for competitors to replicate.

Direction: As Checkout continues to grow, its ability to deliver better data and insights to customers will grow, too. It is important to understand that yes, while hearing about the “data advantages” purported by every SaaS company ad nauseam gets tiring, in the case of Checkout it is intimately tied to the core value offering (better data, better authorization rates, and more merchant sales). Regarding regulation: I don’t think this advantage grows through time in any significant way. If anything, a head start means that competitors will eventually catch up (there are only so many countries in the world!).

Switching costs: In this section, I want to quickly compare legacy processor switching costs and compare them to Checkout’s. Legacy payment providers tended to have very high switching costs because their solutions were custom integrated into merchants' existing payment stacks. This meant that replacing a provider was a difficult process. Besides the time and money needed to rip and replace the old PSP, there was also the risk that a new provider might not work as well as the previous one. Modern payment providers tend to be less customized and, therefore, theoretically easier to replace (more APIs, fewer custom integrations, etc.). However, switching costs associated with authorization rates, data insights, etc. are enough to make fully changing a lead processor difficult. Therefore, the key difference between legacy and new payment providers' switching costs, in my opinion, is that legacy switching costs were a headache for customers, whereas modern switching costs are more a function of the capabilities of any given processor.

Direction: So long as companies like Adyen and Checkout continue to refine their offering and add more value to customers, the switching costs will remain high. Customers should be happy about this – there is no need to switch if you’re using the best solution!

Growth

The payments world is full of powerful incumbents. Yet, over the past decade, Checkout has somehow grown, and grown a lot. Before digging into what will drive growth over the coming years, I want to take a quick detour to help illustrate what I think drove Checkout’s early success. Feel free to skip the history section if you’re pressed for time.

History: I think Checkout’s early growth is the result of Pousaz making some clever decisions. Specifically, I think he built a solid PSP with good tech and focused on growing within niche industry verticals and geographies. Below, I speculate on four potential historic growth drivers. To be clear: the four points below are largely guesswork, supported by some anecdata, so take this all with a grain of salt.

Niche customers: Today, Checkout serves several blue-chip customers, including Netflix, LinkedIn, BydeDance, and Facebook. However, Checkout hasn't always worked these high-profile, global businesses. If we set the clock back a couple years, Checkout's customer list looks significantly different. Using the Wayback Machine, we see that as recently as 2017, Checkout was serving some large clients like Samsung and Adidas, but didn’t have the massive customers it has today. To grow, it appears that Checkout targeted online, mid-market industries that were underserved by existing providers. These businesses also likely operate with smaller margins than many other online businesses, meaning that higher authorization rates are meaningful. Examples include businesses in online clothing retail, fintech, and travel. Today, it looks like Checkout still has meaningful penetration in these areas.

Niche geographies: In the same way that Checkout targeted underserved industries, the company appears to have pursed a geographic expansion strategy aimed at growing in less-penetrated geographies. Again, using the Wayback Machine, we see that as Opus Payments, Checkout first opened offices in Singapore and Mauritius and soon thereafter established partnerships with acquiring banks in Europe and Africa. Next, Opus created a partnership with “China’s leading acquiring brand.” In early 2011, Opus opened a London office, and rebranded just over a year later as Checkout.com. The next office that Checkout opened was in Dubai, with the goal or serving the MENA region. While London is clearly a financial hub, Asia, the Middle East, and Africa are unusual places to first launch. I suspect that Checkout had slightly less competition in these countries and was therefore able to grow faster than if it was going head-to-head in some more penetrated geographies.

Customization: In a handful of interviews, Pousaz describes how Checkout can be customized for different customer needs. This is in stark contrast to Adyen, which, despite recent industry specialization, has been very reluctant to customize its core solution. I’m not sure exactly how customizable Checkout actually is, but I wouldn’t be surprised if this added flexibility helped win some early clients.

Risky business and pricing: Please, please, please take this with a bigger-than-usual grain of salt. I’m including this section in order to pose a question rather than to describe a fact. So, starting with “risky business.” I’m curious if Checkout serves businesses that other processors tend to avoid. Examples include airlines, gambling, and adult entertainment. It wouldn't be unreasonable for Checkout to pursue this business – thanks in part to a lack of service providers, PSP margins tend to be higher in these industries compared to others. And it would also likely be easy business to win, especially post Wirecard. On the pricing point: I’m curious if Checkout is undercutting other PSPs, like Adyen, to win some large clients. Very little evidence supports this, but it is noteworthy that while traditionally profitable, 2019 marked the first loss (link) for the company since 2013. Are they investing in new products, or taking on business at a loss?

Going forward: Now that Checkout is more established, its growth opportunities have changed. A large part of growth going forward will be a result of Checkout riding the massive e-commerce wave, now with more scale than ever before. Beyond that, I suspect that the company will continue to penetrate existing clients, pursue large enterprise business, and introduce new products. Additionally, if/ when Checkout comes public, it looks like it should be able to increase margins meaningfully.

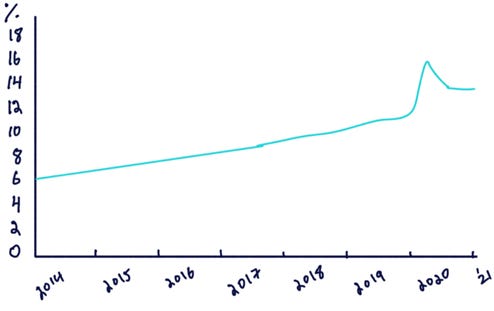

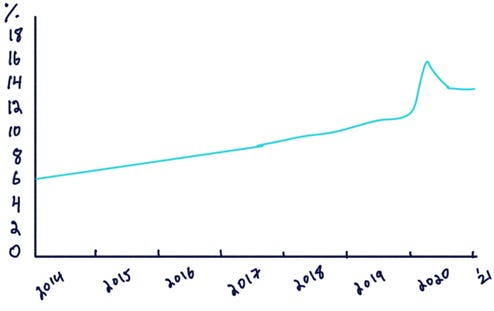

E-commerce: Checkout is an e-commerce first business. As a result, it benefits from the long-term tailwind of businesses moving sales online. The pandemic accelerated e-commerce adoption for both merchants and customers, and I expect the trend to continue. The chart below shows US e-commerce retail sales as a percent of total sales, clearly trending up and to the right.

Source: FRED Enterprise growth: Checkout has been pushing up-market and boasts a number of high-profile customers. Examples of enterprise-scale merchants include Facebook and Netflix. These types of customers provide some social proof for Checkout, which should help the business pitch itself to other enterprise-scale businesses.

Customer penetration: As outlined above, most businesses use multiple payment processors to handle transactions. Based on performance, reliability, conversion, and other factors, the order of these processors can change – meaning that the number three processor can become the number one processor if their solution proves to be best. For those of you familiar with Adyen, this likely sounds familiar, as it is a common component of most theses on the name: further existing client penetration. I suspect the same to be true for Checkout. In fact, Checkout likely has significantly more runway than Adyen, given that it is six years younger and therefore has had less volume migrate to it within existing customers.

New products: As the payments value chain continues to evolve, bundled PSPs like Checkout continue to offer new services. Again, if we look to Adyen to see what Checkout might do next, an obvious step would be getting into issuing and unified commerce. The issuing opportunity is likely going to come sooner rather than later: as of 2018, Checkout.com obtained issuing licenses for both Visa and Mastercard. As of today, I can’t find any Checkout issuing products, though, and I assume the company is still working on their product and strategy for issuing (See Checkout’s description of issuing here). Unified commerce, or handling payments online and in brick-and-mortar locations, seems like a bit more of a stretch for Checkout given its laser-like focus on serving online customers. In the long run, though, I think it makes sense for Checkout to push into unified commerce, given its growing customer set of online and offline retailers (e.g. Adidas).

Margins: Checkout's margin profile is very different than Adyen's, despite operating a similar business. Going forward, especially if/ when Checkout goes public, I would suspect that the company would be able to get better leverage on fixed costs and improve its margin structure. I actually see little reason Checkout's margin structure shouldn't look at least somewhat similar to Adyen's. To help frame the opportunity, consider the following: Adyen expects its long term EBITDA margin to push north of 65% (today around 62%), whereas Checkout’s 2019 gross profit margin was 37% and its operating margin was negative (for the UK entity, the only publicly available filings I could find).

Leadership & culture

Checkout is led by CEO Guillaume Pousaz. He founded Checkout in 2012 and has been leading the company since. As alluded to in the introduction, Pousaz has an uncommon background. Certain "Outsider" traits include that Pousaz is a college dropout, a surfer, and prior to Checkout had relatively limited experience in the payments world. Given Checkout's success, Pousaz's background clearly has not been a problem, and might actually be an asset.

To better understand Pousaz, I’ve read and listened to a number of interviews he has given. In these, he comes across as focused and competitive. He refers to the two (arguably) biggest names in payments, Adyen and Stripe, as competitors – signaling his aspirations. It's certainly good company to keep. Pousaz is also an owner-operator: he is the majority owner of Checkout (as far as I can tell).

Pousaz’s personality is reflected in Checkout’s corporate culture. For a quick read on exactly what defines the business’s culture, we can rely on Checkout’s 2017 Companies House filing, where Checkout describes itself as “A global company with the heart of a startup.” The filing also says that Checkout is “building a unique work environment where our people aspire to solve complex problems and deliver valuable solutions. We believe that excellence can be achieved through a dynamic culture driven by collaboration and teamwork.” Finally, Checkout’s website outlines the company’s three core values: 1) aspire, anything can be built; 2) excel, go above and beyond; and 3) unite, we're greater together. Putting all this together: Pousaz and Checkout are entrepreneurial, driven, and focused on collaboration that solves customers’ problems. My sense is that there is a bit of an underdog mentality that likely unites the employees, too.

To give a little more of a structured breakdown on culture, I’m again using AKO’s culture framework, which I originally applied to my post on AvidXchange.

Adaptability: Checkout's evolution over the last nine years points to significant organizational and cultural adaptability. From California, to Mauritius, to Singapore, the origins of Checkout span the globe. Early customers do, too: From Europe to Asia, Checkout served merchants wherever it could. As the business has grown, Checkout has successfully expanded upmarket – with a product good enough to rival the best.

Customer focus: The "connected payments" offering from Checkout is fundamentally customer focused. The company’s ROI-based sales process creates strong win-win dynamics that place the customer first. Also, ongoing innovation continues to create value for customers (see: The Hub).

Employee focus: Checkout's eye-popping growth has led to associated expansion in the company's headcount. In 2020, the firm doubled from 500 employees to 1,000. In 2021, the CCO, Bradley Riss, expects headcount to increase again, this time by 750 employees (link). The result is that, unsurprisingly, according to the Checkout.com website, 79% of employees have been at Checkout for less than two years. This rapid growth presents real challenges when scaling culture across the organization. Despite this, Checkout has managed employee satisfaction well. Glassdoor reviews give Checkout a 4.7/5 rating. On the positive side of things, reviews highlight a fast-paced environment, employees working on solving real challenges, and physical and mental health support efforts especially during COVID. On the negative side of things, most reviews highlight general growing pains and the heavy lifting associated with bringing new employees onboard. Another negative: Glassdoor reviews suggest that the company doesn't offer equity to employees, which is surprising. Perhaps more senior employees have grants, but it sounds like the majority do not. My take is that as long as Checkout manages the hiring process well and continues to engage and please employees, the company shouldn’t have problems. In order to support this, Checkout has monthly employee engagement surveys, offers employees continuous learning and up-skilling opportunities, and monitors employee NPS (eNPS).

Governance: While Checkout is founder-led, the company has been busy making some very high-profile hires. Some examples: the CTO, Ott Kaukver, was previously at Twilio and before then, Skype. The CRO, Nick Worswick, was previously at WeWork and GrubHub. The CCO, Bradley Riss, comes from Adyen. I realize these hires aren’t directly related to governance, but I think Checkout’s ability to attract high-caliber talent suggests the organization is well run. From a diversity perspective, 33% of leadership team is female, but management roles are all male (as far as I can tell). The company has a number of internal communities that “contribute to diversity, equity, inclusion and belonging at Checkout.com.”

Risks

My biggest concern with Checkout is that what has led to its success might also lead to its demise. Remember, historically, Checkout has served mid-to-large sized enterprises that were using inferior payments partners. However, two competitors are eying this exact market, and these are two real, heavy-weight businesses: Stripe and Adyen. Stripe, while originally focused on the long tail of SMBs, is now providing payments services (and more) to larger businesses. Coming from the other end of the spectrum, Adyen is also looking to grow in the “mid-market” in order to extend its growth. If Stripe and Adyen both attack the mid-market, Checkout’s core business could be seriously challenged. The caveat here, of course, is that payments is a massive market and can support multiple competitors.

Conclusion

Examining the fast-follower dynamic playing out at Checkout is a fascinating case study in the power of copying good ideas. A 1996 quote from Steve Jobs is applicable to Checkout: “good artists copy, great artists steal.” Pousaz, the payments artist, has done an incredible job copying, stealing, and transforming parts of Adyen and other successful payments businesses. Checkout’s unbelievable growth, wide moat, and strong culture are all testament to Pousaz’s vision and the power of emulating what works well.

I wouldn’t be surprised to see Checkout IPO in the next year or two. If that’s the case, I’d love to see a couple of lingering questions answered. These include: How customizable is the product? What does pricing look like vs. peers? How much “risky” business do you process? What do you think of Adyen and Stripe aggressively entering the mid-market?

Thanks for reading! If you have any thoughts or would like to get in touch, you can find me on Twitter or at thesuggestivist@gmail.com

Disclaimer: The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.